.jpg)

We at Ambit are constantly trying to stay ahead of the curve by drowning out the noise and looking ahead. In keeping with our long term investment thesis, we like to stay up to date with not just the present impediments faced by your portfolio companies but also long term disruptions which can hit these companies. Hence we will regularly come out with our thoughts on disruptions in your portfolio companies/ sectors and for the 19th volume of this series we have selected Dr. Lal Pathlabs with a broader focus on the Diagnostics space

This note takes a closer look at challenges facing Dr. Lal Pathlabs and especially the Diagnostics industry and how the company is placed to challenge those.

Dr. Lal Pathlabs – A Resilient Healthcare Brand

Late Dr. Major S.K. Lal, father of the current chairman Dr. Arvind Lal, started an entity named Central Clinical Lab in Delhi in 1949 which went on to set up one of the first private Diagnostics Labs in India. The name was later changed to Dr. Lal Pathlabs in 1995, since that is how Central Labs started to be identified as. Since Dr. Arvind Lal took reins of the business 1977, after his father’s demise, the company has undergone several innovations and pioneered many ‘Industry Firsts’ which made it the resilient Healthcare brand that it is today:

- Launched Thyroid testing in 1982, which was categorized as Nuclear Medicine.

- Adopted various Technological innovations such as using an auto-analyser, hormone-testing equipment and even computerizing the labs, all of which helped streamline and fasten processes.

- Set up the first Franchise Model in Healthcare business in India. The franchisees collected samples which were then sent to country’s central lab for testing.

- Investments in strengthening systems, processes and proper lab governance post appointing a professional management team (including current MD – Dr. Om Prakash Manchanda) in 2005. Lab clusters were assigned under geographical heads. Zonal heads reported to SBU (Strategic Business Unit) heads who in-turn reported to the CEO. A new brand image and marketing plan was also christened.

- Currently DLPL is the world’s biggest tester of Biopsies with ~1,400 Biopsies/ day. They are also the world’s largest in Kidney Biopsies and the only pone with an electron microscope in this part of the globe.

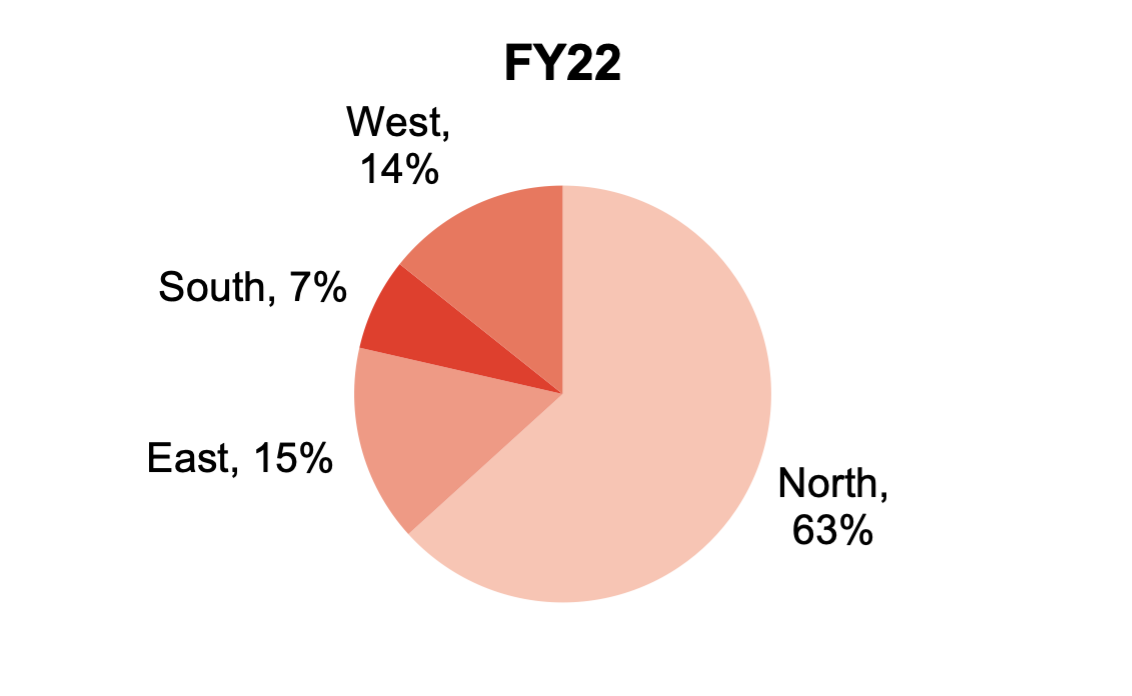

DLPL was predominantly focused in North and East India till a few years back, however, it is now planning to expand – organically and inorganically – into West and South regions where it does not have a much stronger presence. In Sep-21, it acquired Suburban Diagnostic – a leading brand in Maharashtra – for ~Rs925Cr to gain a foothold in the western market. Going ahead, these will be the markets which will contribute meaningfully to its growth, however execution will be the key.

Exhibit 1: North and East still account for 3/4th of revenue, however West and South should pick up in the coming years

Source: Ambit Asset Management, Company

The Evolution of Diagnostics Industry in India

A. Defining Moments of the Past –

In order to understand the disruptions facing DLPL and the industry in India, it is important to understand the evolution of the industry. Diagnostics industry in India is currently ~Rs70,000Cr constituting <10% of the Rs10Lac Cr healthcare industry in India. The industry has gone through three key defining moments that have helped shape the industry:

- Steps towards formalization – Diagnostics, initially, was a fragmented industry which was largely doctor focused and prescription driven, with very limited players. This was the time when a few large players, especially pharma companies, tried to formalize it and ushered in fundamental changes. Companies such as SRL Diagnostics – started by then Ranbaxy promoters Malvinder and Shivinder Singh; and Pathnet – a JV between Dr. Reddy’s and Gribbles Pathology Labs (Australia) came up. It was also the time when high-end tests were introduced and The industry became a little more consumer focused.

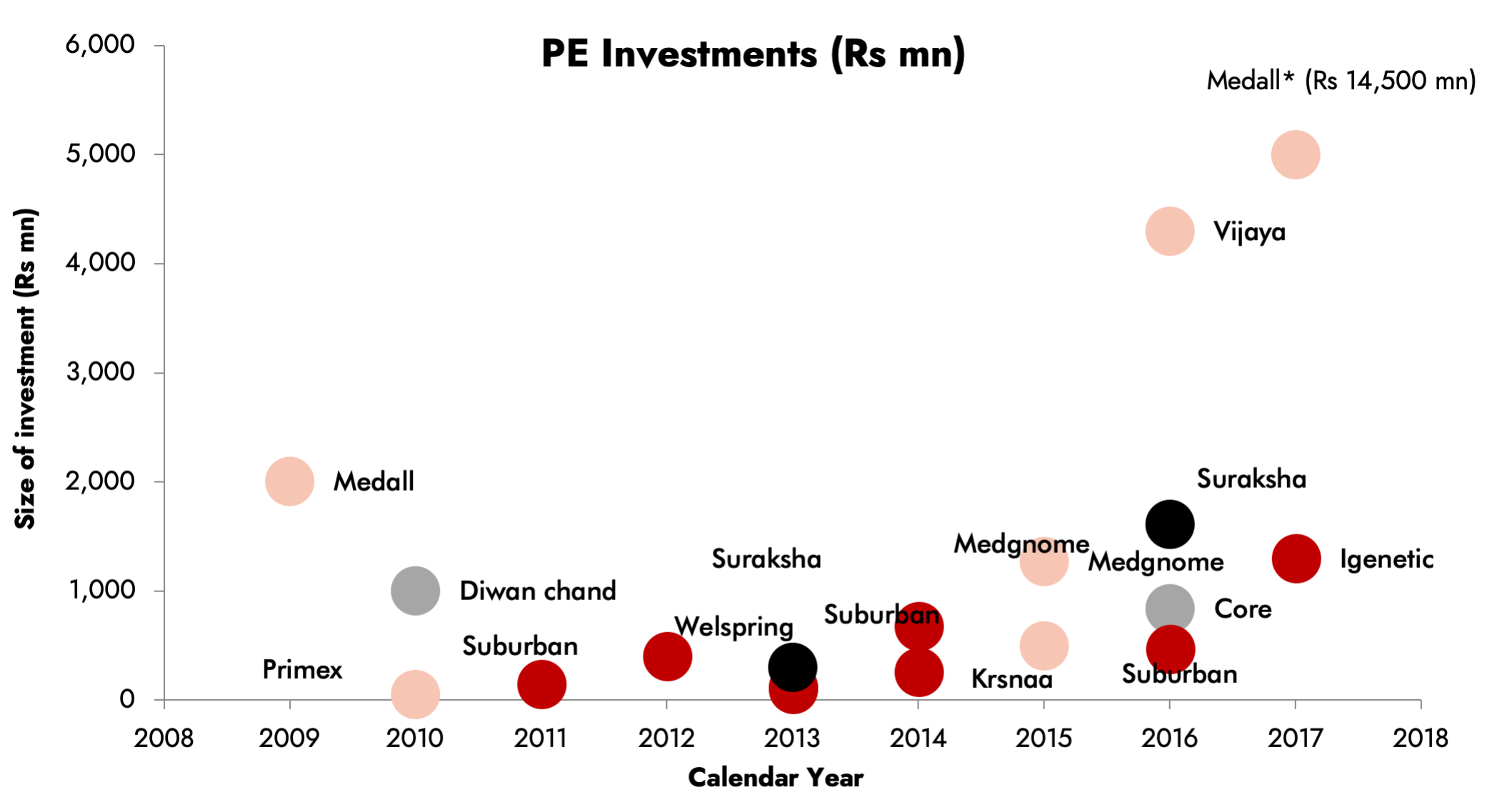

- Influx of Private Equity Funding and Capital Markets listing – PE/VC led funding in early 2000s to mid-2010s was followed by listing of major Diagnostics chain in late 2010s. All of these helped increase visibility of organized Diagnostics chain in the Country. However, it also increased competitive intensity meaningfully, especially in late 2010s when a lot of PE investment flowed into the sector (Refer Exhibit: 2).

- COVID led impetus – Reduced mobility during COVID and huge demand for RT-PCR testing gave rise to Digitization with increase in home collections. A lot of smaller Diagnostics and independent labs witnessed increased profitability and cash flow which led to incremental expansion by them resulting in the current increased competition. Increased health awareness, ease of testing led to an increase in Preventive testing

Exhibit 2: Funding flows from PE players to the tune of USD400mn over 2013-18 with focus on South & West India

Source: Media, Ambit Capital Research,*Investment made in Medall to the tune of ~Rs14,500mn scaled down for visual purposes, Grey indicates northern region, black indicates eastern region, pink indicates – southern region, maroon indicates western region, Includes secondary deals also

B. Industry overview – Story in charts

Exhibit 3: Of ~Rs10tn Healthcare industry in India, Diagnostics constitutes 6-7% share

Source: Ambit Capital Research

Exhibit 4: … of this, Pathology constitutes a larger share and is highly competitive given low entry barriers

Source: Ambit Asset Management, Vijaya Diagnostics DRHP

Exhibit 5: ~50% of Diagnostic industry is dominated by standalone labs / unorganized players…

Source: Ambit Asset Management, Metropolis FY21 AR, Vijaya DRHP

Exhibit 6: …implying very less Market Share for leaders / organized chain vis-à-vis other countries

Source: Ambit Asset Management

Exhibit 7: India has high Out-of-pocket healthcare expenditure implying relatively higher cost sensitivity

Source: Ambit Asset Management, The World Bank data

Exhibit 8: Routine tests (low entry barriers, high margins) currently seeing high price-led competition

Source: Ambit Asset Management *As per estimates

C. Varying Business Models in Indian Diagnostic Industry

- Hub and Spoke Model (B2C) – Diagnostic chains mainly adopt the hub-and-spoke model to extend their catchment area. This model is more prominent in pathology testing services. The components of a hub-and-spoke model typically include a National lab, Regional / Satellite labs and Collection Centers (Refer to Exhibit: 9,10). Collection centres work as spokes and help expand network and transport samples collected to Regional / Satellite labs which have most of the Basic test capabilities. Usually, most of the collection centres are Franchisee owned.

Exhibit 9: An example of a simple Hub-and-Spoke model

Source: Ambit Asset Management, DLPL RHP, CRISIL Research

Exhibit 10: An example of a simple Hub-and-Spoke model

Source: Ambit Asset Management, DLPL RHP, CRISIL Research

- B2B business – The B2B model allows for rapid increase in volumes through samples collected from hospitals, nursing homes and other such establishments. It is leveraged to enter into newer geographies and non-core markets as the initial ramp-up of volume is much easier. Cost is paramount in B2B business. The report can be White-Label or in the Diagnostic Lab’s name with varied pricing.

- Managed Labs – These are the laboratories which are owned by individuals or hospitals whose operations are outsourced to a third party – mostly a larger diagnostic player, who manages the day-to-day operations of the lab with a revenue share agreement. Diagnostic chains due to their wide network benefit from economies of scale and are therefore better equipped to operate these managed labs.

- Public-Private Partnership – The PPP is a type of Managed Lab model. Government hospitals invite bids to operate Diagnostics centres at their hospital, the tenure for which ranges from 2-10 years. The Private Service provider needs to invest or set up Radiology and Pathology labs at the physical premise provided by the authority. The services are provided free of cost to patients referred by government institutes, with the cost being reimbursed by the authorities as per the tender. An annual price escalation may be allowed under the tender but high receivable days is a key risk.

Scanning for Disruptions

1. Competition Galore – During COVID, a number of factors underwent a change which led to an influx of competition in the industry.

- What Transpired and what are the factors that led to increased competition?

- Higher requirement of COVID (RT-PCR) testing – This implied a lot of independent labs and smaller chains were able to scale up quickly and fully utilize their existing infrastructure. Moreover, their ability to cross sell other wellness and ancillary tests led to most of these players reporting life-time high margins (Refer Exhibit: 11). The resultant higher cash flows were utilized to expand business thus creating additional supply and competition in a quick succession.

Exhibit 11: Suburban margins grew sharply in FY21 courtesy COVID testing revenue (50% vs 20% for DLPL)

Source: Ambit Asset Management, Company

Exhibit 12: Some of the price discounts by new entrants in basic testing

|

Mumbai (in Rs) |

DLPL |

Metropolis |

Suburban |

1mg |

MFine |

|

CBC |

250 |

310 |

330 |

299 |

160 |

|

Calcium |

200 |

240 |

260 |

199 |

128 |

|

Glucose fasting |

85 |

90 |

110 |

99 |

34 |

|

Kidney Function test |

850 |

1050 |

670 |

249 |

315 |

|

HbA1c |

550 |

590 |

620 |

299 |

280 |

|

Thyroid profile |

550 |

550 |

810 |

249 |

380 |

|

Lipid profile basic |

200 |

800 |

790 |

249 |

420 |

|

Vitamin D 25-Hydroxy |

1,500 |

1,650 |

1,700 |

349 |

760 |

|

CA 15-3, Serum |

1350 |

1920 |

1440 |

1199 |

760 |

|

HIV 1 RNA Quantitative |

5,000 |

5,500 |

5,460 |

3,832 |

N/A |

Source: Ambit Asset Management, Company

- Increased home collections – Higher preference for Home collection implied quicker ramp-up for new entrants – despite limited physical infrastructure – leveraging the tech enabled back-end. E-pharmacies and Health tech platforms, which saw an increased traction during the same period saw overlapping synergies with strong cash flows and margins which would help plug the gap in their existing cash burning businesses.

- Change in the decision maker / influencer – Earlier, doctors were key decision makers but with increased awareness, requirement for preventive testing and increased Digital adoption, brands were able to target customers directly and gain mind-share. This was especially true of Tier-1/ Metros instead compared to Tier-2/3 cities.

This led to an influx of new competition, especially in Routine / Semi-specialized testing which are largely automated and high margin with limited manual intervention and hence have low entry barriers. Growing pie of wellness testing which is not driven by Doctor prescriptions became an easy target making that segment more susceptible to competition and price discounts by new entrants (Refer to Exhibit: 12). These new entrants which saw a synergistic rationale in offering Diagnostic service as the prospect of 20%+ Margins and 30%+ RoI was too lucrative to not target and also helped fund losses in their other businesses.

B. The future roadmap…

Competitive intensity was always present from unorganized as well as PE/VC (external) funded players pre-COVID. However, the current new entrants however are not dependent on external funding but are either backed by deep pocketed corporate houses or established players in the healthcare industry (Refer Exhibit: 14). This remains a key risk to the organized Diagnostics chains in the near term as the entrants’ capacity to burn cash would not be limited by dearth of PE fund, and their near-term strategy will shape the competitive intensity in the near-term. Moreover, Hospital chains – such as Max, Apollo, etc – expanding their retail Diagnostics presence poses a much stronger B2C competition, albeit in their specific geography. However, over the medium to longer term, we expect following trends to play out –

- Operating within their niche – Players will eventually find and operate within their niche – segment or market – and drive synergies there. For eg. Thyrocare in Thyroid testing, Vijaya Diagnostics in AP/Telangana and integrated centres, Krsnaa in B2G testing (PPP Model). But this journey is long as seen in Thyrocare’s case which took 10-15 years to attain mass scale. (70k samples / 3L tests a day).

- Growth in Tier 2/3 towns – Most of the competition is currently limited to Metros / Tier-1 cities. Top 20 cities in India account for 50% of Diagnostics hence huge untapped potential in Tier2/3 market. DLPL, for eg, has alluded to this being a major growth driver.

- Service over price – While price is an important factor, especially in a cost conscious country like India where majority of the healthcare expense is still out-of-pocket. However, service and quality are equally important in healthcare, lacking which one’s expenses could be much higher (in case of incorrect reading or repeat tests).

- Innovation and newer use cases: Several use cases in the Industry are still untouched and there is potential for lot of innovation beyond annual health check-up packages. Programs such as Skin Care, Arthritis, etc are slowly being introduced and these can provide newer avenues for growth (Refer to Exhibit: 13).

Exhibit 13: Healthcare packages related to specific ailments such as Skin Care, Arthritis, Cardic, etc are now being offered

Source: Ambit Asset Management, Company

Exhibit 14: Some deep pocketed players that are present or have recently ventured into Diagnostics

Source: Ambit Asset Management, Google Images

2. Suburban integration remains a key –

DLPL has been trying to replicate its success in North India in the South and Western regions – especially West – which is a large and lucrative market. With organic growth efforts yielding limited results in west, inorganic foray was imperative and when the opportunity to acquire Suburban Diagnostics came up, DLPL did not shy away. But it would be fair to say that till now the outcome has not gone as planned. Earlier and faster than expected decline in COVID testing revenue and longer than expected time in rationalization and stabilizing the asset have resulted in slower ramp up than management’s expectation.

Management has highlighted that focus initially will be on growth with margins ramping up automatically with operating leverage. The company will follow a twin-brand strategy in West with DLPL focusing on B2B Hospital business and Suburban taking the lead on B2C front.

While Dr. Lal has successfully executed in North India, it is yet to be seen if they can replicate that success in other geographies. Any further delay in execution may drag overall operating performance.

Exhibit 15: Strong presence in MMR/Maharashtra meant Suburban was an ideal asset for DLPL

Source: Ambit Asset Management, Company *: 150 Collection centres and 44 Labs

Exhibit 16: Higher share of COVID testing revenue for SUB compared to DLPL leading to slower revenue recovery

Source: Ambit Asset Management, Company

3. Disrupting the key moat of incumbents – Similar to branded pharma, doctor prescription is an important moat for incumbents in Diagnostic industry as well.Patients in India usually go by the Doctor’s prescription for Diagnostic labs given the quality and reliability of the reports. A patient would usually not deviate from the prescription as that may imply repeat testing and in-turn higher expenses, especially when there is an anomaly in reading. Also, lower awareness in Tier 2/3 towns implies higher influence of Doctor referrals there. But this status quo may get disrupted –

- Entry of Pharma companies – Pathkind Labs by Mankind Pharma and Lupin Diagnostics by Lupin are two examples of Pharma companies venturing into Diagnostics. Domestic Pharma companies like these two have a strong doctor connect courtesy their MR network. Therefore, there is a high likelihood of them trying to disrupt that channel and moat of the incumbents

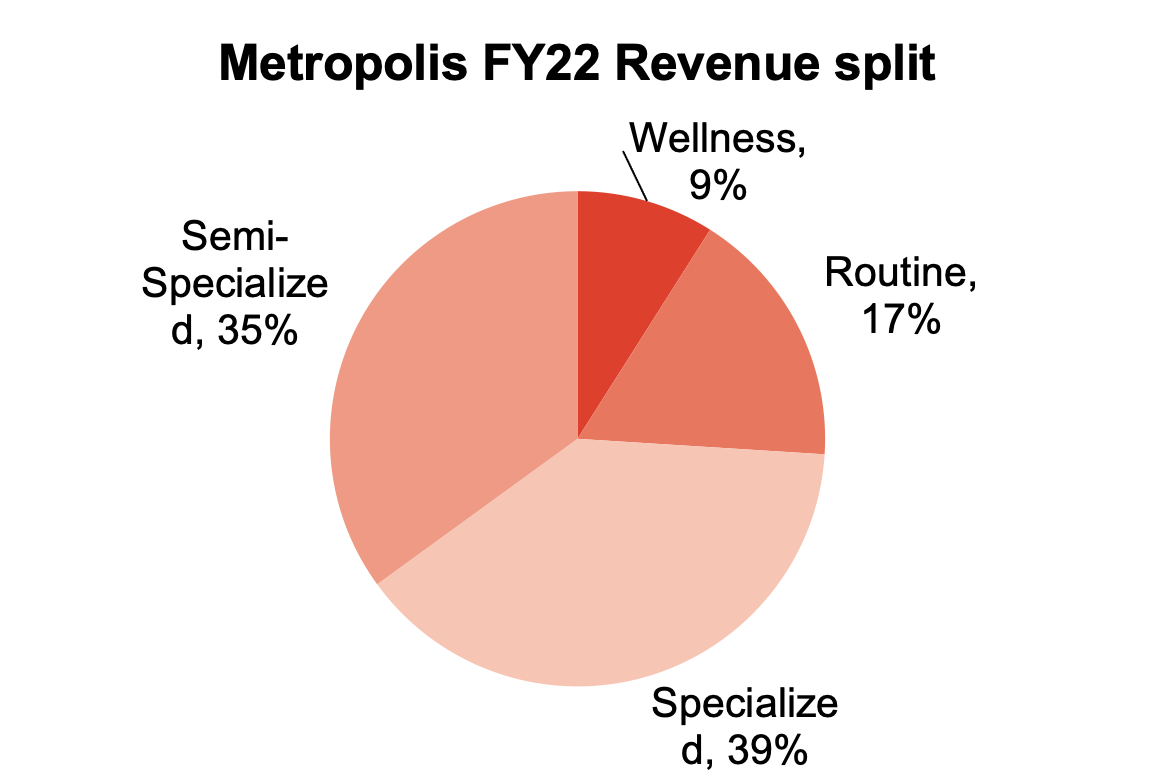

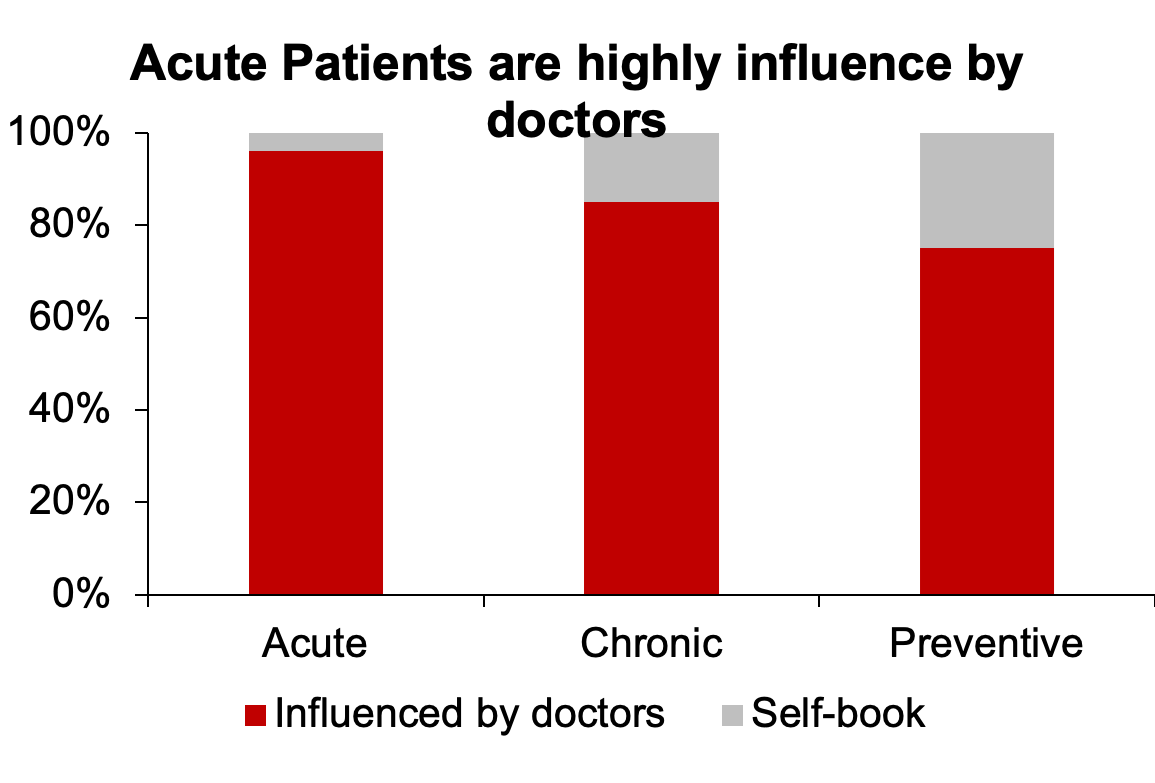

- Less impact of Doctor referrals on Wellness / Preventive testing –Currently Wellness testing constitutes ~10% of the industry, however it is slated to grow at a much faster rate as people become more health conscious. This segment has limited to no doctor influence as compared to acute / Chronic tests (Refer Exhibit: 18) and hence much easier to target for new entrants.

Exhibit 17: Low share of wellness testing in India vis-à-vis DM (40%+) which provides huge scope for growth…

Source: Ambit Asset Management, Company

Exhibit 18: … in a segment which may not hold much doctor influence

Source: Metropolis presentation; Ambit Asset Management

It is very difficult to crate and scale a quality healthcare brand in India. While new entrants might be able to attract patients based on pricing and doctors based on relationships, it’ll be very difficult to build trust which established brands like DLPL have spent decades on. The core of this trust is superior service and consistent quality, which doctors can trust. This is not the first instance of pharma companies entering Diagnostics space, which makes us believe that there is more to do over and above Doctor connects.

4. Government subsidized tests or price caps – It is difficult to implement and monitor regulations in Diagnostics given the highly fragmented and unorganized nature of clinics and diagnostic labs (~1Lac). Indian Council of Medical Research (ICMR) formulated an Essential Diagnostics List (EDL) in 2019, similar to the National List of Essential Medicines (NLEM). It notified Operational, infrastructural and regulatory guidelines and identified ~160 essential tests which will be offered at most Public healthcare centres, but did not include any pricing regulation, yet.

However, it is difficult to come out with a standard price for tests as it is a service as opposed to medicine which is a product. There are various factors which determine cost, such as Use of Syringe or Catheter, Place of collection (home or walk/in), Phlebo / technician cost, etc.

Various government agencies, however, have made noise around regulating prices and standardization of quality. Introduction of a price cap on these basic tests remains a key risk as Basic / Routine tests constitute >60% of revenue for DLPL and even higher on profitability. Standalone instances of Price control may also impact companies in near-term. For instance, Delhi state Government, a few years back capped the prices for dengue tests. Similarly, it will now be offering 450 tests for free in all government hospitals starting Jan-1. Even during COVID, Government had kept price control on RT-PCR tests. However, organized Diagnostics chains – especially B2C focused – can charge patients for service component such as – Digital access, home collection, convenience fee, etc. and make up for the difference.

5. Fast evolving business model – The existing business models (Refer to Business Models section) which largely relied on front-end presence and physical network may get disrupted in the light of increased digitalization.

- New entrants need not invest heavily in physical infrastructure or outsource to franchisee. Direct to Consumer approach with focus on Home collection implies flexible scale up / down as the Phlebotomist can be redeployed to higher volume areas. However, there is downside to this model in regards to heightened consumer expectation.

- Integrated healthcare services provider will have a funnel of services and users. They can offer other integrated healthcare services (Pharmacy, consultation, Therapy, etc.) on one platform and make money there. This may in-turn push prices further down.

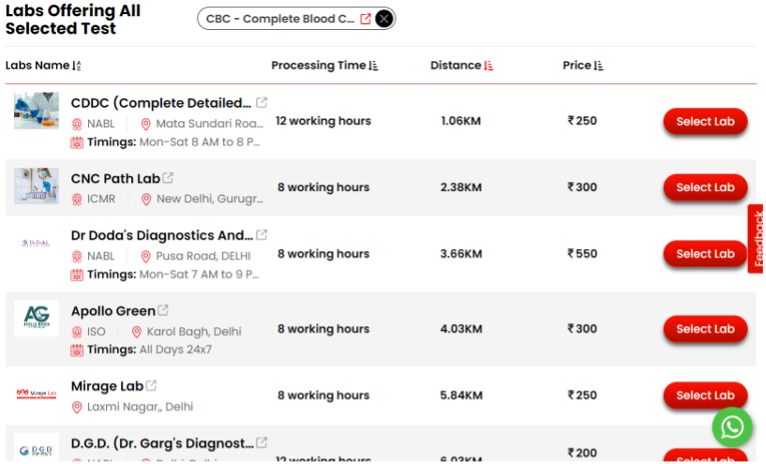

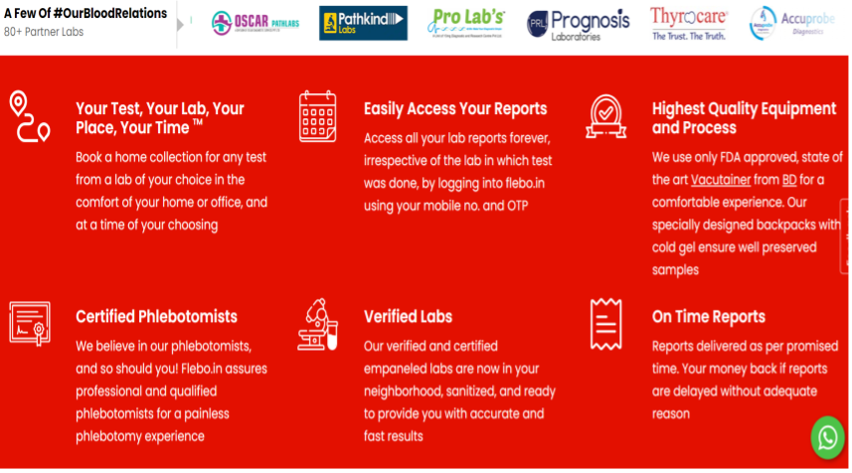

- Marketplaces such as flebo.in – with a network of >100 Phlebo – allow patients to book a Phlebo for home collection of sample and pick a lab of their choice where they would want to get the sample tested (Refer to Exhibit: 19, 20). In addition to empowering patients, such platforms will also help increase visibility of smaller labs that want to increase their utilization.

Often, there has been a parlance drawn – at least in capital markets – between Diagnostic Healthcare and Consumer industry. We believe Convenience, Price and Quality are 3 important parameters in healthcare industry of which Quality is paramount and that’s what differentiates this industry from Consumer industry. A wrong reading in a Biopsy testing is not the same as late Pizza delivery where waving off delivery charges would solve the problem. Most of the new entrants have been targeting Convenience and Affordability. Home collection by a Phlebotomist may depend on various factors such as complexity of tests, patient’s co-operation, in addition to external factors, all of which may make it difficult to meet heightened user expectation for convenience and time. In our view, long-term survivors and winners will have to be agile and adapt to changing business models while not compromising on Quality. DLPL has consciously tried to refrain from price. It is focusing on building a strong Tech back end which will help provide competitive pricing and convenience while maintain margins and Quality.

Exhibit 19: A range of tests at flebo.in

Source: Ambit Asset Management, flebo.in

Exhibit 20: which can be tested at any of the 80+ partner lab

Source: Ambit Asset Management, flebo.in

6. Technological Disruptions and increased traction in Point-of-Care testing – Technological innovation may lead to development of non-invasive diagnostic tests that can be performed by patients or physicians at various locations and without the need of a free-standing clinical lab or a phlebotomist. Some examples of these include blood sugar test using blood sugar monitor, Cholesterol test strips, Infectious disease testing kits (HIV, Hepatitis, TB, etc.).

Such innovations may lead to price cuts or even redundancy of basic routine tests. Similar trend was witnessed in RT-PCR testing during the COVID Omicron wave. RAT or Rapid-Antigen Test which could be easily performed at home, replaced RT-PCR testing and severely impacted revenue of Diagnostics players in Q4FY22. Also, specialized tests becoming Routine as a result of these technological innovations would affect the premium charged on such tests by Diagnostic chains.

Additionally, Lab equipment manufacturers – that currently sell to Diagnostic Labs – may focus more on marketing POC Lab Equipment to physicians by selling test kits approved for home use to both physicians and patients. This may negatively affect the market for lab testing services.

Case in point – 1: Siemens Healthineers

Siemens Healthineers – which provides majority of lab equipment in India – has various POC testing solutions for Cardiac, Coagulation, Urinalysis, Diabetes, etc. in addition to Informatics and Data Management solutions.

Exhibit 21: Aina Blood Monitoring System – world’s first smart phone based diagnostic system enabling the detection and management of chronic diseases. It offers a broad range of tests such as HbA1c, Glucose, Haemoglobin and lipid profile on a single platform

Source: Ambit Asset Management, Company

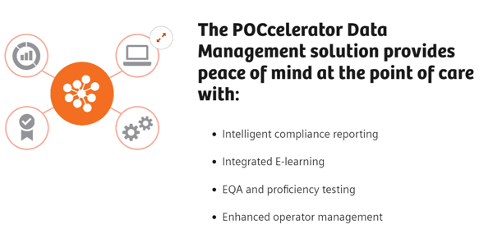

Exhibit 22: POC Data Management Solution can help track and monitor Data at a centralized location from numerous POC testing devices

Source: Ambit Asset Management, Company

Exhibit 23: Xprecia Stride™ Coagulation Analyzer is used for PT/INR testing that helps diagnose the cause of bleeding or clotting disorders

Source: Ambit Asset Management, Company

Case in point – 2: Sanskriti PoC KIOSKS

Sanskritech is a POC testing startup in which Mylab Discovery Solutions acquired majority. Sanskritech is the developer of Swayam which is a portable diagnostic and telemedicine POC system that can be used to create a small lab anywhere. It can perform 70+ tests for Respiratory Diseases, Vector Borne Diseases, Heart, Urine Tests, Liver, Vitamin D, HIV, etc. and generate a report within 15 minutes. Patients can also consult a doctor in real-time.

Exhibit 24: Swayam – a portable diagnostic and telemedicine Point-of-Care system –can be used to create a small lab

Source: Ambit Asset Management, Company

Case in point – 3: If Edison type technology actually comes about?

19 Year Old Elizabeth Holmes founded Theranos in 2003. Theranos' business model was based around the idea to devise blood tests that required merely drops of blood (a pinprick on your finger), using proprietary technology. It would be able to detect medical conditions like cancer and high cholesterol. These claims were later proved to be wrong and Elizabeth has been convicted for fraud. Interestingly, Elzabeth Holmes had also filed a patent application for a wearable device that would be able administer medication, monitor patients' blood and subsequently adjust the dosage. If devices like these are indeed developed by someone else in the near future, it has the potential of disrupting the industry.

7. Capital allocation pitfalls –

-

- Inorganic foray – Given the negative working capital nature of the business, DLPL’s post-tax cash generation is ~100% of EBITDA. Given the asset light business model, most of this is available for redeployment. Any hasty deployment of the cash flow generated in the future in inorganic opportunities with limited synergistic benefits or even foray in non-core healthcare services, may end dragging the superior return ratios of the company.

- International expansion – DLPL has negligible international presence at present with only 2 of the 197 labs outside India. It is present in Nepal and Bangladesh and receives samples for testing in India from 20+ countries across Asia, Middle East and Africa. The management’s current focus is on expansion in the domestic market considering relatively low Diagnostic and Healthcare penetration. However, over the longer term (next decade), any international expansion whether organically or inorganically may pose serious challenge if not executed properly.

CONCLUSION

Healthcare industry is at an inflection point in India, with huge scope for growth. It is not easy to create or even displace a strong healthcare brand in India. DLPL has a legacy of 75+ years. We like the strong Brand and Franchise, coupled with an experienced Management team which DLPL has built over the years and expect the company to be a major beneficiary of increased healthcare spending in the country.

The future of Diagnostics industry in India would depend on (1) Willingness and capacity of new players to burn cash and their Long Term strategy (2) Pickup in the overall healthcare spending and infrastructure of the country (3) Agility and nimble-footedness of players to adjust to changing trends and business models. Going ahead, we feel (a) Turnaround of Suburban asset (b) Expansion in Tier-2 and 3 towns (c) Replicating the success of Delhi (NCR) in other geographies will be the key factors to watch out for DLPL.